For small businesses, getting paid has always been a balancing act. You want to make things easy for your customers, but you also need systems that are reliable, trackable, and fast. You also want simplicity, not tracking fifteen different channels, each with its own systems for CRM and transaction data. For a long time, those goals were at odds.

That’s changing.

Much like embedded finance reshaped e-commerce by letting customers pay without leaving the experience, today’s mobile payment tools are doing the same thing in everyday business interactions. Payment is no longer a separate step at the end—it’s becoming part of the service itself.

For small businesses, that shift is quietly improving cash flow, reducing administrative work, and increasing close rates in ways that weren’t possible just a few years ago.

The Old Way: Friction City

Not long ago, most small businesses relied on payment methods that worked—but not particularly well.

Cash was immediate, but hard to track, easy to misplace, and increasingly out of step with how customers prefer to pay. Card payments, while more common, often meant manual entry, standalone terminals, or waiting to process transactions later. Sometimes invoicing filled the gaps, but introduced delays between when the work was done and when money came in.

Managing transactions across these different methods was rarely seamless. Records were scattered, visibility was limited, and the payment experience itself often felt clunky for customers.

When Payment Becomes the Experience

Modern payment tools allow businesses to collect payment at the exact moment a service is delivered or a sale is made. Instead of sending someone home with an invoice, you can complete the transaction while the value is still fresh and the intent to pay is highest.

This shift from delayed billing to real-time payment may seem minor, but it has major downstream effects. It shortens the cash cycle, reduces accounts receivable, and removes a layer of follow-up work that used to be unavoidable.

It also aligns with broader trends in POS and SaaS systems, where businesses rely on integrated platforms that combine payments, customer management, and reporting into a single workflow. The goal is to simplify operations overall.

Does Your Phone Have Service?

One of the clearest shifts in modern payments is how quickly businesses can move from service to transaction, thanks to personal devices.

Pay-by-link is often the simplest place to start. Instead of generating an invoice and waiting, a business can send a payment link via text or email as soon as a job is completed—or even before it begins. The customer clicks, chooses their payment method, and pays in seconds. The real advantage isn’t the technology itself, but the timing: payment happens while both parties are still engaged, reducing delays and improving cash flow.

Tap-to-pay brings that same immediacy to in-person transactions. Businesses can accept contactless payments directly on a smartphone, without dedicated hardware or manual entry later. Customers tap their card or digital wallet and move on. It’s fast, familiar, and aligned with how people already pay, removing hesitation and helping close more transactions on the spot.

Digital wallets tie it all together. Customers increasingly expect to pay with stored credentials and biometric authentication, whether online or in person. When those options aren’t available, even small inconveniences can slow things down or sink a sale.

Recurring Payments: Stable Billing, Low Overhead

Another area where modern payment tools are making a difference is recurring billing.

For businesses that operate on retainers, subscriptions, or ongoing service agreements, automated payments remove the need to repeatedly request and process payments each cycle. Once set up, the system handles billing in the background.

This creates more predictable revenue and reduces administrative overhead. It also aligns with the broader shift toward subscription-based models across industries, where consistent, recurring revenue is increasingly valued over one-time transactions.

Even for businesses that don’t think of themselves as “subscription-based,” there are often opportunities to introduce recurring structures that benefit both the business and the customer.

The New Challenge: Omnichannel Overwhelm

If the old problem was friction, the new one is fragmentation and complexity burden. Businesses today aren’t short on payment options—they’re often juggling too many. One tool for invoicing, another for tap-to-pay, another for online checkout, and another for traditional payments.

It’s a headache to manage and get actionable insights from payment data. Payment data can be scattered and less useful, and reporting turns into a manual process just to piece together what’s actually happening. That can turn off businesses, especially smaller merchants with less bandwidth for juggling.

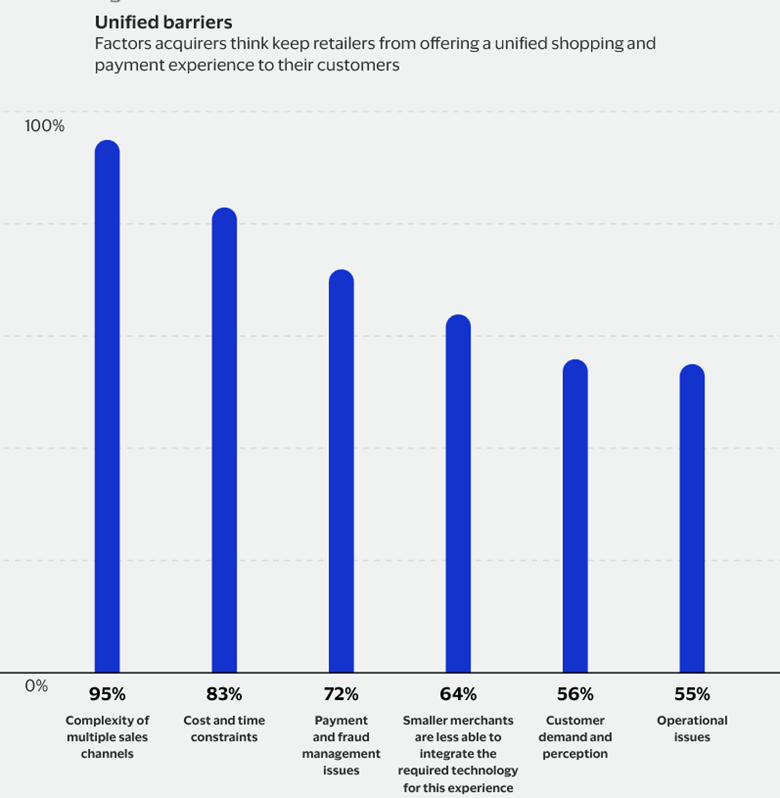

PYMNTS Intelligence surveyed 200 acquirers (institutions like COCARD that connect merchants with banks), and found the following:

Source: PYMNTS Intelligence

“According to 95% of acquirers, the complexity of managing multiple sales channels is a key challenge for merchants, primarily resulting from difficulties in matching online and in-store payment experiences. Cost and time constraints follow, at 83%.”

Additionally, 64% of acquirers said that smaller merchants are less able to integrate the tech needed for a seamless omnichannel experience

One System, Not Five

If fragmentation is the problem, consolidation is the solution.

Omnichannel setups often leave businesses juggling disconnected tools for invoicing, in-person payments, online checkout, and reporting. The result is scattered data and time spent piecing together what should be clear.

An integrated platform brings everything into one system. Payments, customer data, and reporting all live in one place, giving businesses a real-time view without the manual work.

Instead of managing multiple tools, small businesses can focus on using the data and running the business.

COCARD: Staying Ahead of Modern Payments

Mobile and flexible payment options are now the standard, even for small businesses. As expectations shift, merchants need solutions that keep transactions fast, simple, and reliable without adding operational complexity.

COCARD brings these capabilities together in a single platform—from pay-by-link and tap-to-pay to digital wallets and recurring billing—helping businesses streamline payments and improve cash flow. Even better, we integrate payment data in one consolidated suite for better CRM and analytics.

As the payments landscape continues to evolve, our focus remains the same: giving our partners the tools and support they need to adapt, compete, and grow.

Get in touch today to modernize your payment experience.