In last year’s regulatory outlook, the payments industry was still digesting the early signals of a second Trump administration: a hollowed-out CFPB, a pause on aggressive fee rules, and a widely questioned proposal to cap credit card interest rates at 10%.

As we move into 2026, the contours of the new regulatory approach are clearer. What we’re seeing is not a clean sweep of deregulation, but a more selective approach: legacy financial institutions are more attractive targets, while emerging payment technologies—especially crypto—are given room to run.

For payment processors, ISOs, and fintech platforms, we have some key takeaways. The rules are looser in many places, especially for crypto and other emerging technologies, but credit regulations remain unpredictable.

The 10% Credit Card APR Cap: Populism Meets Reality

Donald Trump’s repeated comments about capping credit card interest rates at 10% continue to loom over the industry, even in the absence of concrete action. The proposal is unusual for a Republican administration and has attracted bipartisan populist support, including praise from progressive lawmakers who rarely agree with Trump on anything.

Bernie Sanders and Josh Hawley even introduced legislation to put the cap into action, but it never made it past introduction. Still, as of early 2026, there is no serious legislative push behind the idea.

Here’s why we think a cap is unlikely in 2026:

- Implementing a nationwide APR cap would require Congress to pass legislation.

- The cap would likely face constitutional challenges under interstate banking and usury doctrines, and would fundamentally alter credit underwriting models.

- Issuers would respond by tightening credit, cutting rewards, and pushing marginal borrowers out of the system entirely.

- Industry lobbying groups are (predictably) dead-set against it.

The more important takeaway is not whether the cap happens (it probably won’t), but why it keeps resurfacing. Credit card interest has become a major symbol of consumer frustration in a high-rate environment.

Even in a deregulatory era, that makes card issuers vulnerable to targeted intervention. Expect continued hearings, headlines, and pressure on pricing practices, even if a hard cap never happens.

Crypto’s Back, Back Again

If traditional credit remains in the crosshairs, crypto has experienced a full regulatory thaw. Under Biden, crypto payments were stuck in limbo: too big to ignore, but too risky to embrace. Enforcement-first regulation by the SEC and a hostile posture from banking regulators effectively froze experimentation at the edges of the payment stack.

Under Trump, that posture has reversed. In 2025, the United States enacted the GENIUS Act, the first federal stablecoin framework that defines how payment-focused stablecoins can operate, requires 1:1 backing with liquid assets, and assigns bank regulators oversight rather than the SEC or CFTC. With clearer (or at least quieter) federal oversight, dollar-pegged tokens are being integrated into cross-border settlement, B2B payments, and merchant ecosystems.

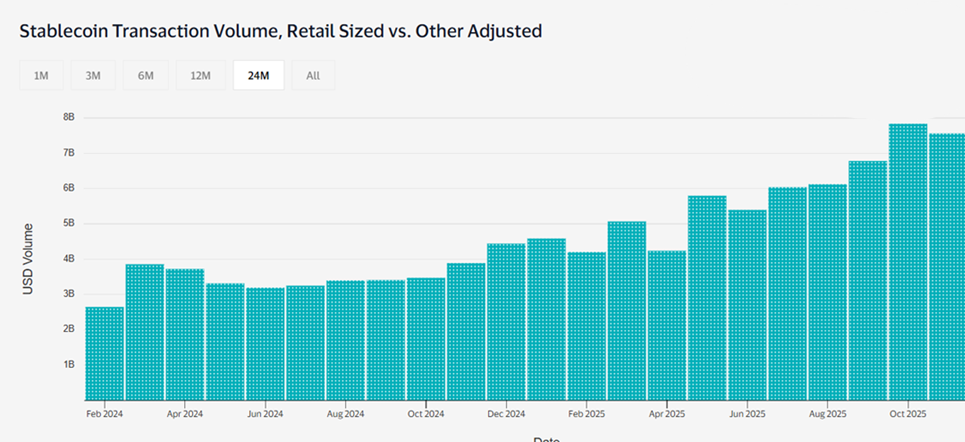

Stablecoins: Slowly Hitting Checkout

Source: Visa Analytics

That legislation has begun to reshape crypto’s use case. Stablecoin transaction volumes, particularly those tied to regulated issuers, soared in 2025. For retail payments and stablecoins, these changes matter more than for speculative trading. Stablecoins are finally emerging as a credible payment rail.

Major payment networks like Visa have rolled out stablecoin settlement between institutions, enabling near-continuous movement, often at lower costs than legacy systems. While still a small percentage of total volume, retail payments with stablecoins more than doubled in 2025.

This isn’t yet a wholesale replacement for Visa or Mastercard in everyday retail payments, but the backend infrastructure is evolving rapidly. Regulators have signaled that innovation and competitiveness are priorities, particularly when digital asset rails can reduce friction and global liquidity costs.

Looking ahead, legislative momentum is building on broader crypto market rules: a draft bill introduced in the Senate aims to clarify how digital assets are categorized and address some enforcement gaps left by the GENIUS Act. These moves are likely to further anchor crypto’s role in payments and cross-border commerce in 2026.

Trump vs. the Fed: DOJ Enters the Fray

If 2025 was Trump’s trade year, from lobbing tariffs to inking new agreements, 2026 will likely be the Year of the Fed. Running beneath nearly every financial prediction for 2026 is the escalating conflict between the White House and the Federal Reserve.

What began as rhetorical attacks on interest rate policy has now crossed into direct institutional pressure. In January 2026, the Department of Justice served grand jury subpoenas on the Federal Reserve in connection with Chair Jerome Powell’s congressional testimony.

Powell has publicly characterized the investigation as politically motivated, arguing that it coincides with sustained pressure from the Trump administration to force faster and deeper interest rate cuts. This represents a sharp break from modern norms around central bank independence, and it has injected new volatility into rate expectations.

This spat could have a real impact on the payments industry. Interest rates directly influence credit card APRs, consumer borrowing behavior, and delinquency trends. They also have a real impact on aggregate retail spending. Much like the 10% APR cap, Trump’s public campaign against the Fed reframes high card rates as a policy choice rather than a market outcome.

So far, Trump has few allies in Congress for attacking the Fed. Many congresspeople in his own party have spoken out, and central banks around the world have signed an open letter endorsing the Fed’s independence.

Regardless of what happens, the Fed’s future independence has come into question like never before.

Payments Regulation Becomes Fragmented

With federal agencies stepping back from heavy-handed enforcement in some areas, states are filling the gap. Progressive states continue to push consumer protection in lending, payments, and money transmission. More permissive states are rolling out fintech and digital asset charters aimed at attracting innovation. That patchwork increases compliance complexity for national platforms like ours.

At the same time, enforcement risk has shifted toward specific consumer harms. Deceptive pricing, unfair disclosures, and opaque fee structures remain easy targets. Weak enforcement at the federal level doesn’t eliminate legal risk, but redistributes it across states and consumer-protection agencies.

What This Means for Payment Providers in 2026

The payments industry is navigating a phase where adaptability matters most. Stablecoin infrastructure and crypto rails present real optionality, and the regulatory landscape has made space for it to bloom. However, political volatility around credit costs and monetary policy, as well as new leadership over the coming years, could quickly change the current outlook.

The most resilient players will be those who diversify payment rails, maximize merchants’ platform functionality and incentives, and can navigate a shifting regulatory landscape.

COCARD: Built for Regulatory Whiplash

In 2026, regulatory certainty is hard to come by. We’re used to that!

At COCARD, we’ve seen regulatory cycles come and go. What hasn’t changed is our focus on flexibility, merchant education, and infrastructure that can adapt as the rules shift.

Whether the future tilts toward crypto-enabled payments, renewed card regulation, or anything else, we’re ready to meet that challenge. Since our launch more than 25 years ago, we created a system that can operate across environments, rather than betting on just one.

Get in touch today to join the winning team.